Int'l Finance 笔记

本文是国际金融管理的笔记,教材是「Eun C. and Resnick B. : International Financial Management, 9th ed」

L0 - Course Overview

L1: Introduction to International Finance & International Monetary System

L2 – 4: concentrate on exchange rates

L5: focuses on foreign currency derivatives

L6 & 7: delves into exchange rate exposure of firms and the steps to mitigate its impact

L8: looks at recent trends in international equity markets and international investments

L9: addresses global cost-of-capital and sourcing equity & debt globally and political risk

L10: discusses international capital budgeting

L1 - Intro & IMS

Costs of Globalisation:

- exchange rate

- large tariffs

- subsidize

Prevalent Exchange Rate System

- Currency Union / Dollarization

- Currency Board

- Truly Fixed ER

- Adjustable Peg

- Crawling Peg

- Basket Peg

- Target Zone or Band

- Managed Float

- Free Float

The Gold Standard (1873-1913)

The Gold Standard

- Countries fixed an official gold price

- free convertibility between domestic money and gold

- e.g. 1 ounce = USD 20.67

- The gold price is “mint parity” (determines exchange rate)

- National currency is only issued with gold backing

For Example:

- USD is pegged to gold at $20.67 per oz

- British pound is pegged to gold at £4.2474 per oz

- Therefore, $20.67 = £ 4.2474 (£1 = $4.8665)

Arbitrage Profits (if £1 = $4)

- Buy gold at £4.2474

- Sell gold at $20.67

- Convert at $4 = £1, Get £5.1675

- Profit = £(5.1675-4.2474) = £0.9201

- Note: Do the reverse and you will incur a loss of $3.68

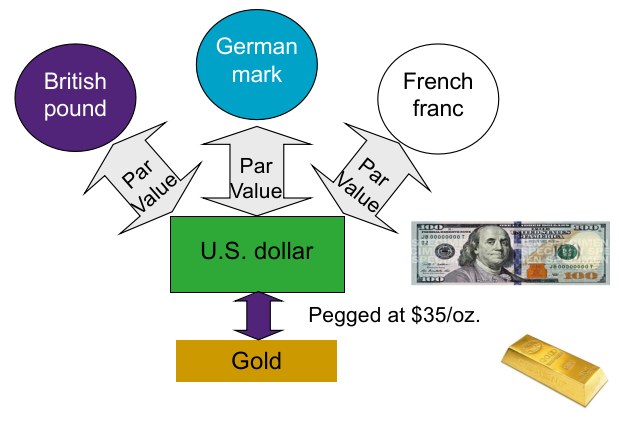

Bretton-Woods (1944-1973)

Bretton-Woods

- USD was fixed in terms of gold (USD 35 per ounce)

- Other countries fixed their currency relative to the USD

- Allowed to vary between ± 1% of the “par value”

- US did not declare any official parity

- Fed was never under any obligation to intervene

Triffin Paradox: Conflict between economic growth (and hence growing need for reserves) and credibility of covertibility

- Crisis of confidence in the US’s ability to meet its obligations

- diverging fiscal, monetary policies and external shocks caused the system’s demise

- In 1968 two tier pricing system was created

- August 1971 USD devalued to $42/ounce and the “gold window” was closed

- In 1973, the Bretton-Woods system collapsed

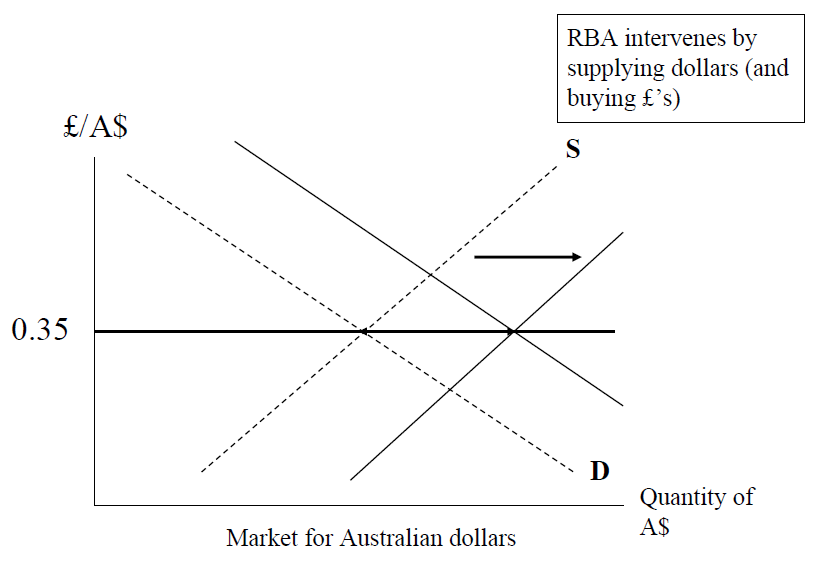

The Floating Rate Standard (1973-1984)

exchange rate is determined entirely by forces of supply and demand

Central banks had the obligation to intervene to prevent “disorderly conditions”

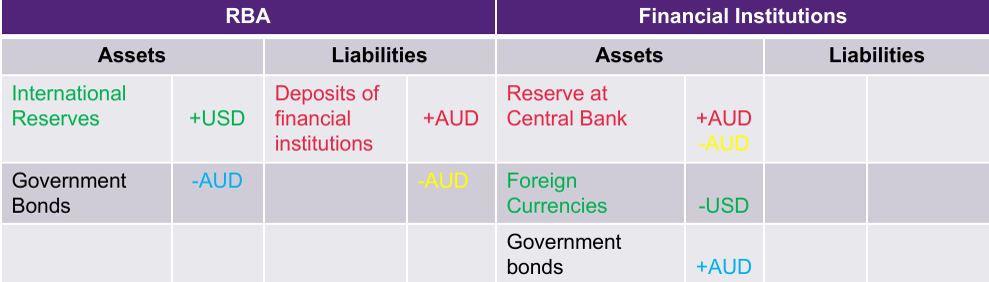

Central Bank's Balance Sheet

to avoid appreciation of AUD

RBA sell AUD and buy USD or foreign assets from financial institutions

it affects the money supply (non-sterilised)

RBA then swap this foreign asset with the government bonds (sterilised)

RBA effectively changes composition of the assets

from foreign asset to domestic asset

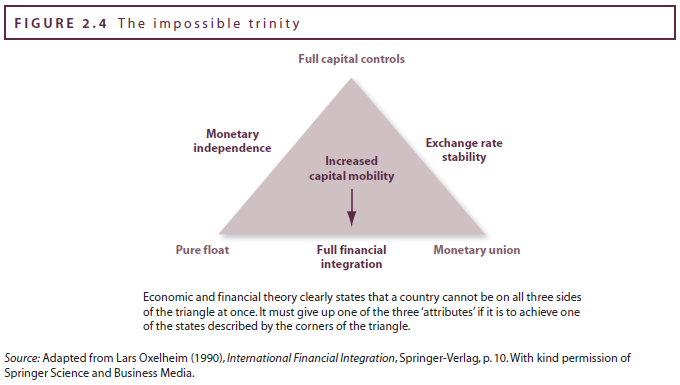

Impossible Trinity

Three Goals (must give up on one)

- Exchange Rate stability

- Full Financial Integration (free flow of capital)

- Monetary independence (of domestic policies)

Example Country

- Pure Float: USA

- Monetary Union: EU

- Full Capital Controls: China

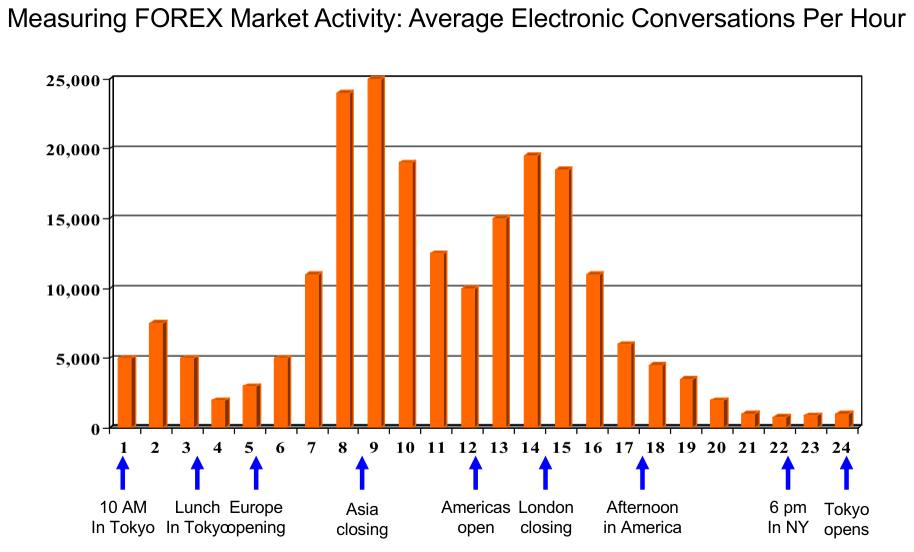

L2 - The Foreign Exchange Markets (FOREX)

Settlement Risk

Settlement Risk: the possibility that one or more parties will fail to deliver on the terms of a contract at the agreed-upon time

Netting: aggregating two or more obligations to achieve a reduced net obligation

Netting Example:

- CBA owes Citigroup $10 billion

- Citigroup owes CBA $5 billion

- Citigroup owes Construction Bank $5 billion

- Construction Bank owes CBA $5 billion

- Gross payments: $10 + $5 + $5 + $5 = $25 billion

- Netting: $0 transaction value

FX Activities

Hedging: transfer exchange rate risk inherent in foreign currency transactions

Speculation: leaves one open to exchange rate fluctuations (aims to make a profit)

Arbitrage: take advantage of inconsistent prices to make risk free profits (unlikely to last long)

- Spatial (or Locational) Arbitrage

- Triangular Arbitrage

- Covered Interest Arbitrage

FX Rates and Quotations

Spot Rate: The exchange rate at which trades are executed immediately in the interbank market.

Value Date (for a spot transaction): the date on which parties actually receive the funds they have purchased

- usually occurs two business days after the deal is made

Direct Quote: Home currency per unit of Foreign currency (FC)

- AUD/€ quote is 1.6003

Indirect Quote: Foreign currency per unit of Home currency

- €/AUD quote is 0.6249

Note that in all cases, the reciprocal of a direct quote is an indirect quote:

American terms: US$/FC

European terms: FC/US$

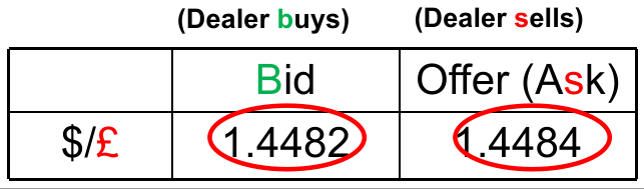

Bid - Ask Prices

Bid Price: Dealer BUY FC from you

Ask Price: Dealer SELL FC to you

Ask Price > Bid Price (the difference is the Bid-Ask spread)

Bid = 1.4482 $/£

- Dealer buys £ for $ at the Bid

- Client sells £ for $

- Dealer will buy £1,000,000 sell $1,448,200

Sell = 1.4484 $/£

- Dealer sells £ for $ at the Ask

- Client buys £ for $

- Dealer will sell £1,000,000 buy $1,448,400

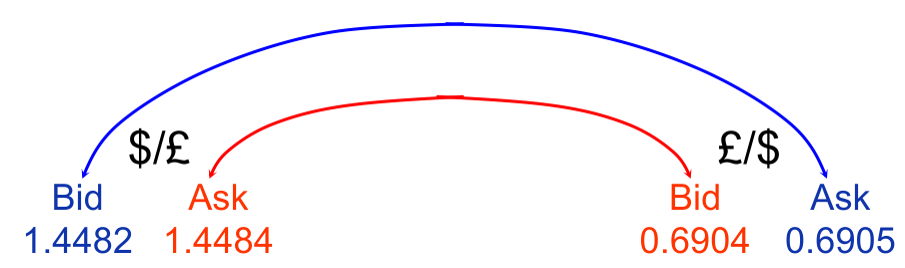

A direct bid (ask) is the reciprocal of an indirect ask (bid)

- Bid-ask quote for AUD/€ = 1.6003 – 1.6499

- Bid-ask quote for €/AUD = 0.6061 – 0.6249

Cross Rates

Many currency pairs are only inactively traded, so their exchange rate is determined through their relationship to a widely traded third currency

For Example:

- Australian dollar = A

- Danish kroner = DKr7.0575/US$

- Then A$/Dkr = (A) / (DKr7.0575/US$) = A$0.2186/Dkr

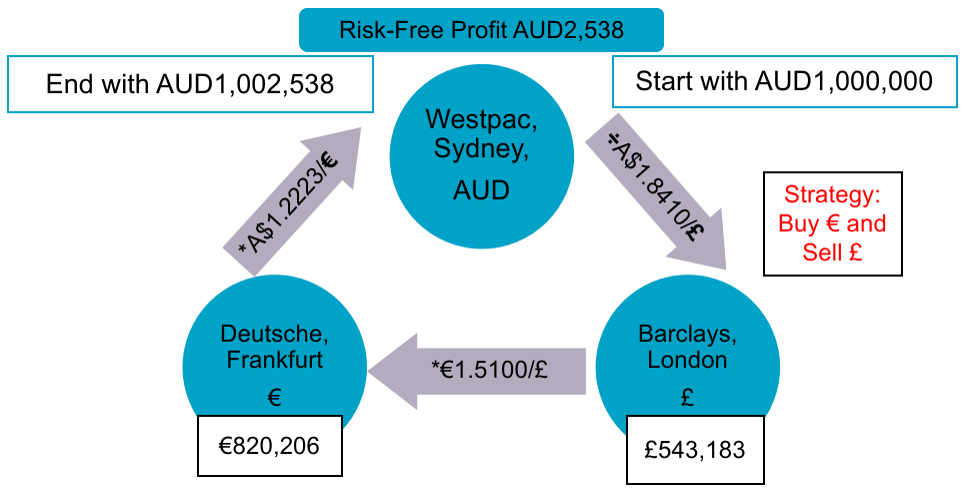

Triangular Arbitrage

- Barclays Bank: A$1.8410/£

- Westpac Bank: A$1.2223/€

- Deutsche Bank: €1.5100/£

- Cross Rate: (A$1.8410/£) / (A$1.2223/€) = €1.5062/£

- Cross Rate < €1.5100/£ (£ Overvalued at Deutsche Bank)

- Strategy: Buy € and Sell £

Cross Rates (Bid - Ask Rate)

- AUD: A$1.5455 - A$1.7158/USD

- DKK: DKr7.0680 - DKr8.1280/USD

- Bid = (A$1.5455/USD) / (DKr8.1280/USD) = A$0.1901/DKr

- Ask = (A$1.7158/USD) / (DKr7.0680/USD) = A$0.2428/DKr

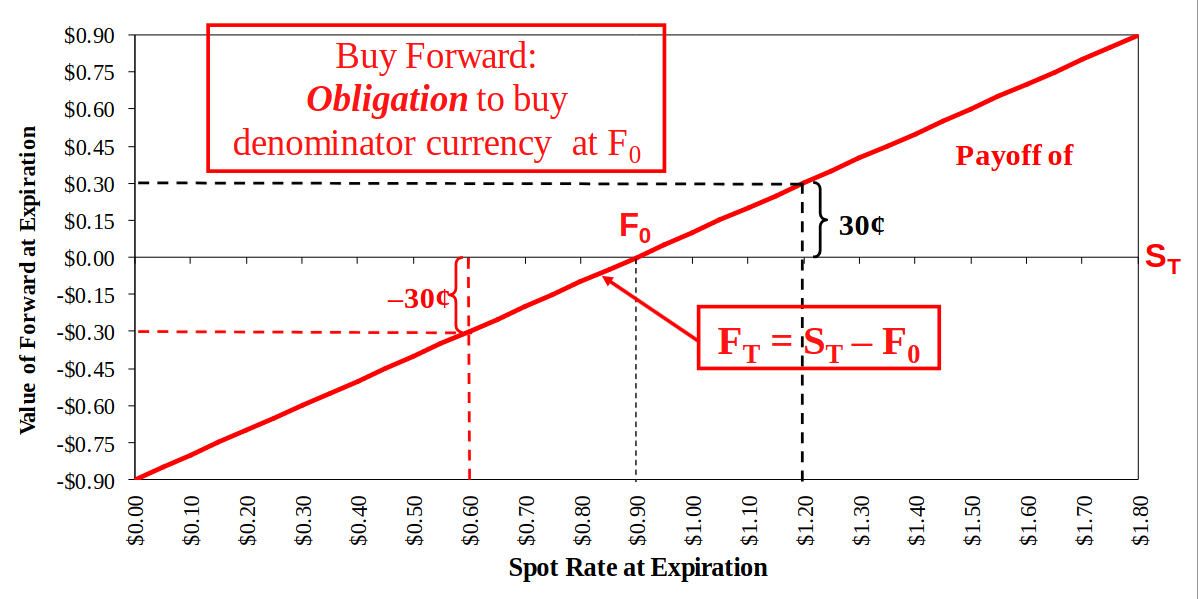

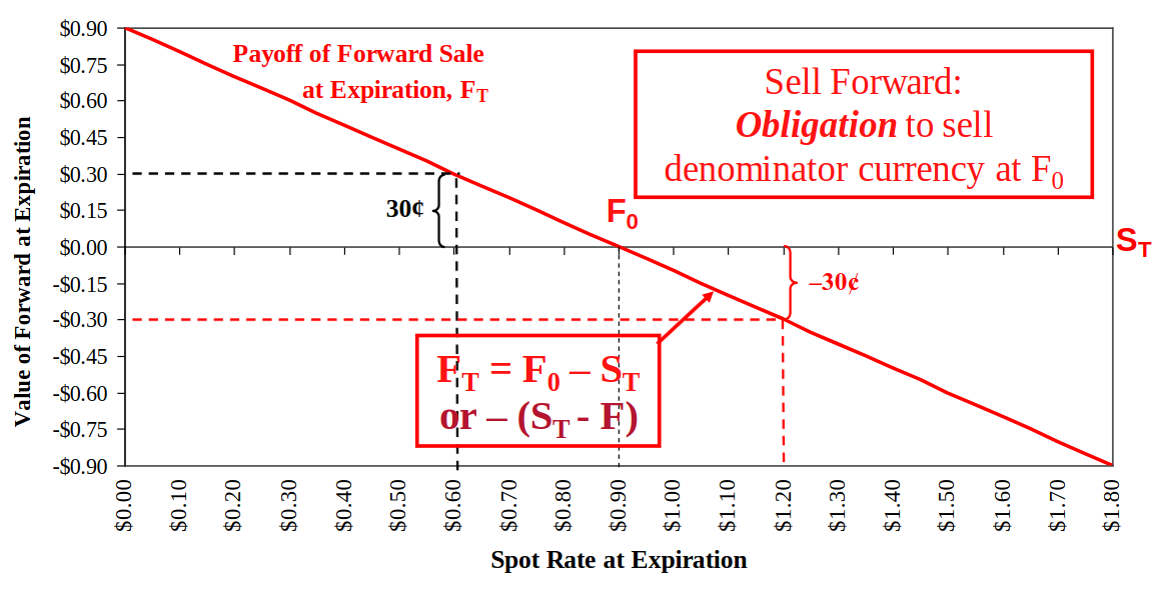

Forward Contracts

Forward Contracts: a rate that is agreed upon today, but settled further into the future

Three ways to express forward rates:

- Outright quotes (either direct or indirect)

- Points to be added or subtracted from spot rate

- Annualized percentage forward premium or discount

Outright quotes

Currencies which are more (less) expensive to buy forward are at a premium (discount)

For the denominator currency, Forward > Spot implies a premium of foreign currency forward

- S = 0.9077 $/SF, = 0.9129 $/SF

- The forward Swiss franc is more expensive to buy

- The forward Swiss franc is trading at a premium to the spot Swiss franc (relative to the dollar)

Swap Rates

Swap Rates: the difference between the forward rate and the spot rate

FX traders usually quote forward rates in terms of points

- A point is the last digit of a quotation

- A point is equal to 0.0001 of most currencies

- JPY is quoted only to two decimal places (0.01)

Bid Points > Ask Points: Subtract the points from the spot rate (to get the outright forward quote)

- forward discount

Bid Points < Ask Points: Add the points to the spot rate (to get the outright forward quote)

- forward premium

Example (European Terms, Sfr/$):

- Spot: 1.5625 - 1.5635

- One month forward: 58 - 56

- Three months forward: 175 - 169

- Six months forward: 342 - 334

- F (1 month)

- Bid = 1.5625 - 0.0058 = 1.5567

- Ask = 1.5635 - 0.0056 = 1.5579

- F (3 month)

- Bid = 1.5625 - 0.0175 = 1.5450

- Ask = 1.5635 - 0.0169 = 1.5466

- F (6 month)

- Bid = 1.5625 - 0.0342 = 1.5283

- Ask = 1.5635 - 0.0334 = 1.5301

Annualized Percentage Forward Premium / Discount

- p > 0: annualised premium of the denominator currency

- p < 0: annualised discount of the denominator currency

- N: maturity of the forward contract (or number of days forward)

For exchange rate: USD/AUD

- If F > S then the currency is trading at a premium

- E.g. One AUD buys more USD in the forward market than in the spot market

- If ascending between bid/offer (i.e., 23 -24 one-month swap points) then forward price will be higher than the current spot price

- If F < S then the currency is trading at a discount

- E.g. One AUD buys less USD in the forward market than in the spot market

- If descending between bid/offer (i.e., 58 - 56 one-month swap points) then forward price will be lower than the current spot price

- If F = S then market is relatively flat

For Example:

- Spot = 0.8772 $/€

- = 0.8785 $/€

- = 0.8806 $/€

- = 0.8891 $/€

- Euro is more expensive in the forward market

- The forward Euro is at a premium

Change in the Spot Exchange Rates

- At t-1: A

- At t: A

- Change: (1.335 / 1.8445) - 1 = -27.62%

- the USD has depreciated relative to the A$ by 27.62%

- At t-1: 1 / (A

- At t: 1 / (A

- Change: (0.7491 / 0.5422) - 1 = 38.16%

- the A$ has appreciated relative to the USD by 38.16%

L3 - Parity Conditions

Parity Conditions: exchange rate is a pair of currencies. Our task - Link this pair with another pair (better if observable)

Parity conditions rely on ARBITRAGE to hold: If they are the same thing, they must cost the same

The derivation of these conditions requires the assumption of Perfect Capital Markets (PCM)

- no transaction costs

- no taxes

- complete certainty

Purchasing Power Parity and Low of One Price

Purchasing Power Parity (PPP)

- based on the notion of arbitrage across goods markets

- given by the Law of One Price (LOP)

- Violations of PPP occur in the short run, but PPP tends to hold in the long run (several years)

Law of One Price (LOP) states that the price of an identical good should be the same in all markets (assuming no transactions costs)

Internal purchasing power = external purchasing power

- A can of coke should cost the same in Australia as it does in Thailand

LOP Example

- Coca-cola: Aus = $4.25/bottle, UK = £2.5/bottle

- Spot rate ($/£) = 1.70

- Buy for $4.25, or flies to the UK and buy for $4.25 × (1£ / $1.7) = £2.5

- The “PPP” exchange rate = ($4.25/bottle) / (£2.5/bottle) = $1.7/£1

Big Mac costs SKr61.29 in Sweden and $5.69 in the US, is SKr overvalued or undervalued if the actual exchange rate is Skr10.45/$1?

SKr61.29 × ($1 / Skr10.45) = $5.865 > $5.69

Therefore Skr overvaluation

Absolute PPP

Absolute PPP

- less extreme form of the Law of One Price

- the price of a basket of goods would be the same in each market

Relative Purchasing Power Parity (Relative PPP)

Relative PPP claims that exchange rate movements should exactly offset any inflation differential between two countries

(Minus 1 from both sides)

Relative PPP implies that the change in the exchange rate will offset the difference between the relative inflation of two countries.

Therefore the above can be approximated as:

- : %change in exchange rates

- : %change in A's levels

- : %change in B's levels

Applications of Relative PPP:

- Forecasting future spot exchange rates

- Calculating appreciation in "real" exchange rates

Relative PPP Example

Given inflation rates of 5% and 10% in Australia and the UK respectively, what is the prediction of PPP with regards to $A/GBP exchange rate?

(0.05 - 0.10) / (1 + 0.10) = -4.5%

If current spot rate is /GBP)?

$1.6/£ × (1 + 0.05) / (1 + 0.1) = $1.53/£

Real Exchange Rate

- When E = 1

- denominator currency is valued correctly

- Competitiveness of this country is unaltered

- When E < 1

- denominator currency is undervalued

- Competitiveness of the denominator country improves

- When E > 1

- denominator currency is overvalued

- Competitiveness of the denominator country deteriorates

Intl Fisher Effect (Fisher-open)

Fisher Effect:

Note: this requires a forecast of the future rate of inflation, not what inflation has been in the past

International Fisher Effect: the spot exchange rate should change to adjust for differences in interest rates between two countries

Interest Rate Parity (IRP)

Interest rate parity (IRP): an arbitrage condition that provides the linkage between the foreign exchange markets and the international money markets

In general, the currency trading at a forward premium (discount) is the one from the country with the lower (higher) interest rate

The approximate form of IRP

- % forward premium = diff in interest rates

Basic idea: Two alternative ways to transform from currency A at time 0 to currency B at time 1 should earn the same return.

Suppose the 3-month money market rate:

- 8%p.a. (2% for 3-months) in the Australia

- 4%p.a. (1% for 3-months) in Switzerland

- the spot exchange rate is SFr1.48/$

The 3-month forward rate must be SFr1.4655/$ to prevent arbitrage opportunities (i.e., interest rate parity must hold)

- F(3m,SFr/AUD) = (SFr1.48/AUD) * (1+0.01SFr) / (1+0.02AUD) = SFr1.4655/$

TODO

L4 - Balance of Payments

The Balance of Payments (BOP) is a statistical record of the flow of all of the payments between the residents of a country and the rest of the world in a given year.

Current Account

- Net exports/imports of goods and services

- Balance of Trade

- Net Income

- investment income from direct portfolio investment

- employee compensation

- Net transfers

- sums sent home by migrant and permanent workers abroad

Capital Account

- Capital transfers related to purchase and sale of fixed assets such as real estate

Financial Account

- Net foreign direct investment

- Net portfolio investment

- Other financial items

Net Errors and Omissions

- Missing data such as illegal transfers

Reserves and Related Items

- Changes in official monetary reserves including gold and foreign exchange reserves

The Current Account (CA)

CA = goods and services + unilateral transfers

CA is divided into 3 sub-categories:

- Merchandise Trade: physical goods like beef, cars etc.

- Services: interest payments, dividends, consulting etc.

- Unilateral transfers: foreign aid, wages repatriated

CA = Exports (X) - Imports (M)

- CA Deficit: M > X (CA < 0)

- CA Surplus: M < X (CA > 0)

CA Balance = Change in Net Foreign Wealth / Assets

The Capital Account (KA) / Financial Account

KA includes all short- and long-term financial transactions pertaining to both international trade and flows associated with portfolio shifts (stocks, bonds etc.)

The two main categories:

- Portfolio investment

- Direct investment

- takeover or acquiring a substantial portion of a foreign company

KA = Capital Inflow (cr) - Capital outflow (dr)

KA balance = Sum of portfolio investment and direct investment

CA and KA Example

Dell sells $20 mil of computers to Komatsu, a Japanese manufacturer of construction and mining equipment. Komatsu transfers dollars from its dollar-denominated bank account at Citibank in New York? What are the credit and debit items on the US balance of payments?

- Computer exports (CA): $20 mil (cr)

- Citibank foreign deposits decrease (KA outflow): $20 mil (dr)

LVMH, a French luxury goods buys EUR1.5 mil of consulting services from Boston Consulting Group (BCG). The firm writes a check on its euro-denominated bank account at different Paris Bank, BNP Paribas. What are the credit and debit items on the French balance of payments?

- Purchase of consulting services (CA): EUR1.5 mil (dr)

- BNP deposits (KA): EUR1.5 mil (cr)

Indonesian resident invested in Japanese bonds. Each year, she receives Yen500,000 coupon payments. These payments are deposited into her Tokyo Bank account. What re the credit and debit items on Indonesian BOP?

- Coupon receipts from Japanese Treasury (CA): Yen500,000 (cr)

- Tokyo Bank, foreign deposits (KA): Yen500,000 (dr)

Japanese firm gifts $2 million to a US University to create an endowed chair professor. The firm finances the gift by selling US Treasury Bonds. What are the debit and credit items on the Japanese BOP?

- Gift (CA): $2 mil (dr)

- Import Good Will

- Sale of US Treasury Bonds (KA): $2 mil (cr)

CA = -KA (This will hold approximately for floating rate countries)

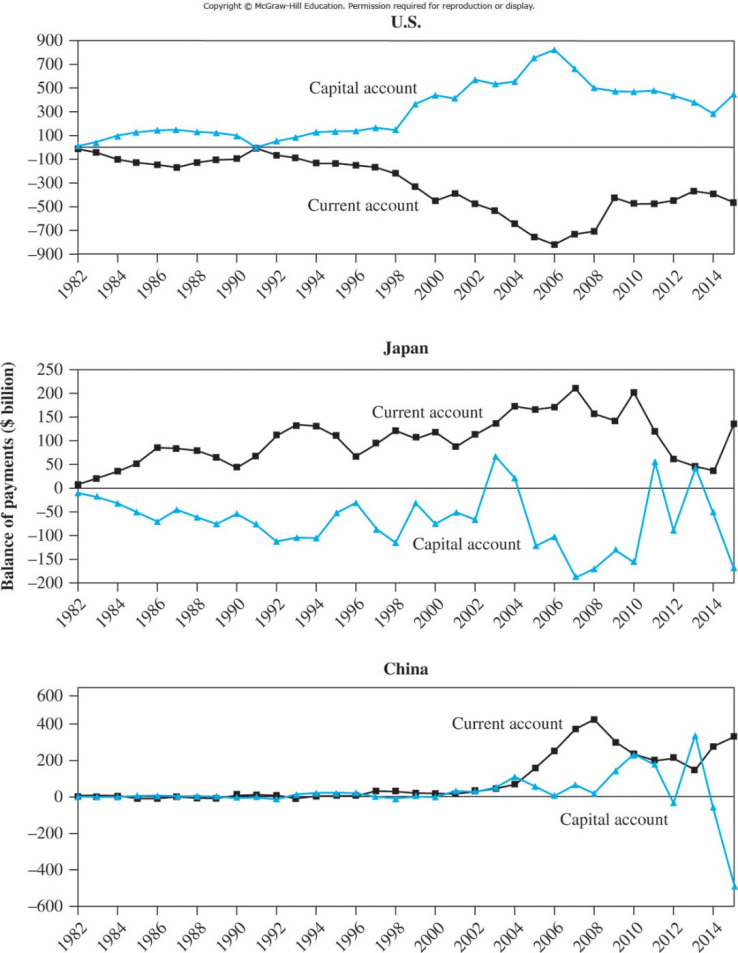

Current & Capital Accounts (1982-2015)

The Other Accounts

- Net Errors and Omissions (Balancing Item)

- account for statistical errors and/or untraceable monies within a country

- Official Reserves - total reserves held by official monetary authorities within a country

- Typically comprised of major currencies that are used in international trade and financial transactions and reserve accounts (SDRs) held at the IMF

- Important account for fixed-rate regime countries

- For floating rate regime countries, such as the U.S., official reserves relatively unimportant

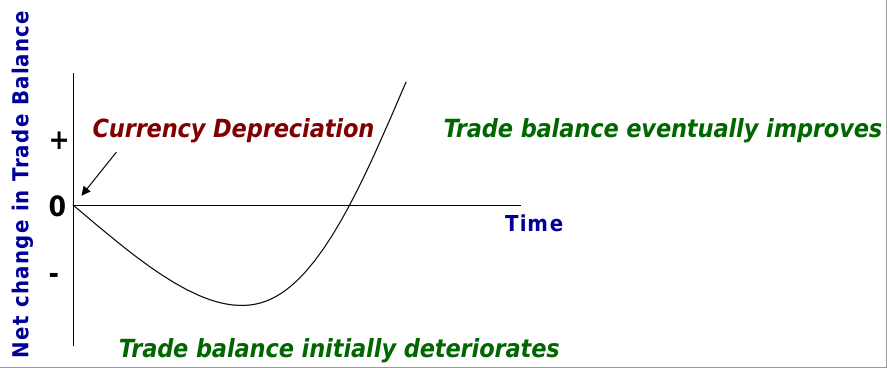

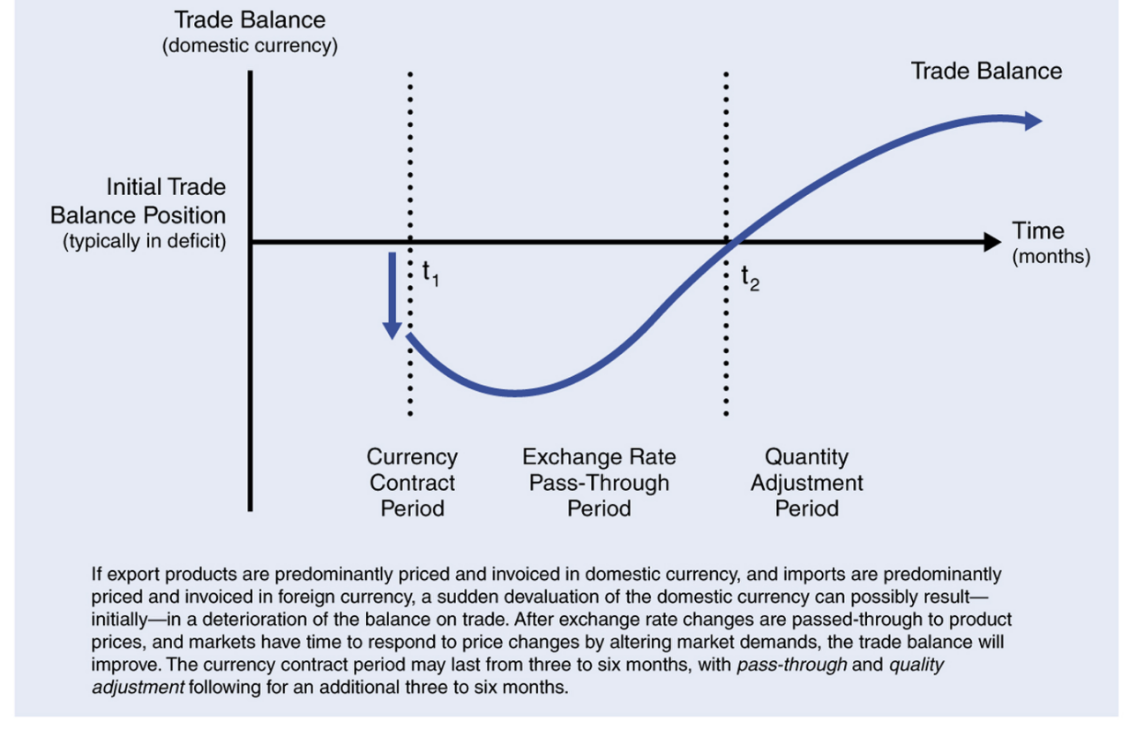

The Trade and Devaluation: J-Curve

J-Curve

- A real depreciation makes imports look expensive and exports competitive

- However, the change in spending patterns takes time

- In the interim, we have nearly the same level of imports and exports

- But the price of imports relative to domestic output has increased, causing a decline in the trade balance

The J-curve adjustment process

- The currency contract period

- the pass-through period

- the quantity adjustment period

Export (X) - Import (M) =

Natural resource curse (Dutch disease)

- Demand for a particular product pushes up the demand for the currencies causing real appreciation

- Exports from other industries lose competitiveness (crowd-out effect)

- Temporary current account surplus might lead to persistent current account deficit

- This is the problem for resource rich countries (Norway, Saudi, Timor Leste)

Solution: Sovereign wealth fund (set up a fund and buy international asset)

- Public Investment Fund (Saudi Arabia)

- Government Pension Fund of Norway

Private Savings = National Income – Consumption – Taxes = Y - C - T

PS = (C + I + G + X - M) - C - T

(PS – I) + (T – G) = X – M = CA

Savings surplus + Govt. surplus = Exports – Imports = CA balance

CA Deficit = a country is not saving enough to finance its domestic investment + government budget deficit

- represents a collective national decision to consume and invest more than the nation is producing

Sustainability of CA Deficits

- A growing economy can expect to run a current account deficit (CAD)

- Countries that have large investment opportunities can run large current account deficits

- Sometimes it makes sense to borrow abroad temporarily (CA = S – I)

- The absolute level of both savings and investment are important

- A CAD caused by low savings (high consumption spending) is less likely to be sustainable than a CAD because of high investment

- higher investment increases future production capacity and the ability to pay back foreign liabilities

- Composition of Investment Spending is important (CA = X - M)

- The more the investment is in traded goods, then more likely to generate trade surpluses

- The manner in which CA deficits are financed matters

L5 - Foreign Currency Derivatives

Futures vs. Forwards

| Futures Contracts | Forwards Contracts | |

|---|---|---|

| Markets | Prices determined in centralized exchanges | Decentralized inter-bank market |

| Trading Hours | Most trading during exchange hours | Open somewhere around the world |

| Contract Size | Standardized sizes depending on currency | Standard size of $1m etc. & can be tailored |

| Contract Maturity | Fixed delivery dates: 3rd Wed. of March, June, Sept. or Dec. | Fixed maturities (1, 3, 6 or 12 months) or can be tailored to specification |

| Quotation | American terms (US$/FC) | American (US) |

| Settlement | Delivery of underlying fx is feasible, but almost never occurs. Position closed out by taking an offsetting position | Delivery of foreign exchange normally takes place. |

| Security against default | Clearing houses stand behind traders | Assets of bank |

| Required collateral | Margin requirements (“Performance Bond”) | Deposit required if no standing relations with bank |

| Cash flows | Occur daily because of “marking-to-market” feature | No cash flows until forward contract matures |

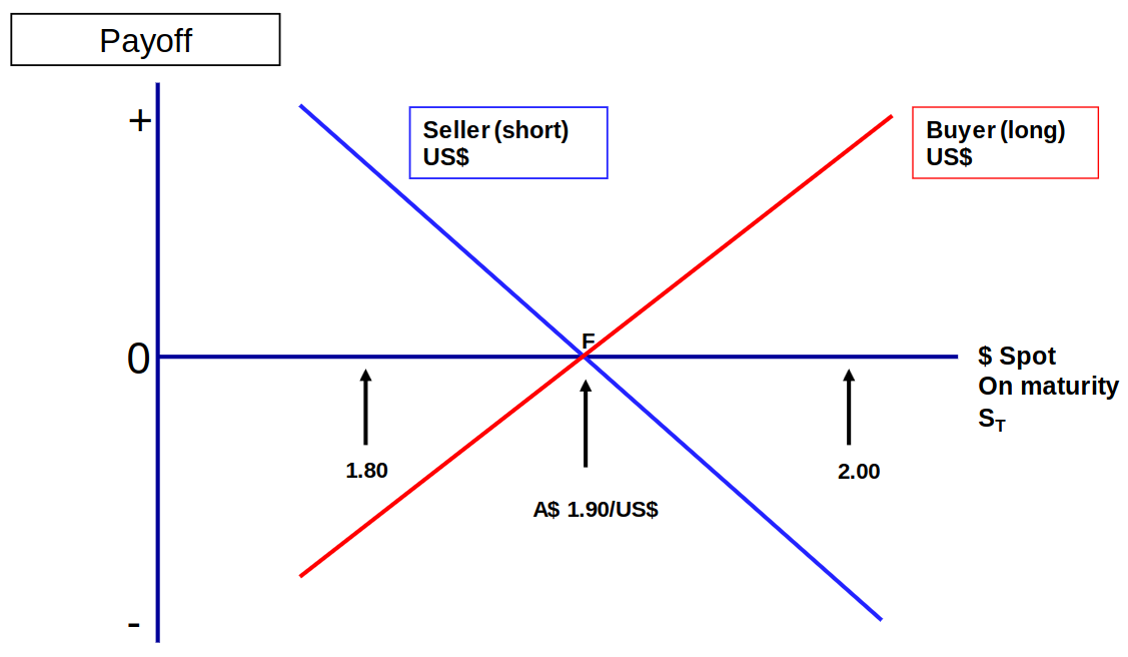

Forwards

At A$ 1.80/US$ - USD 1m will exchange for 1.80 - buyer could default.

At A$ 2.00/US$ - USD 1m will exchange for 2.00 - seller could default.

At A$ 1.90/US$ there is no difference

Forwards Payoff

Value of Forward Purchase at Expiration (US$/SF)

Value of Forward Sale at Expiration (US$/CHF)

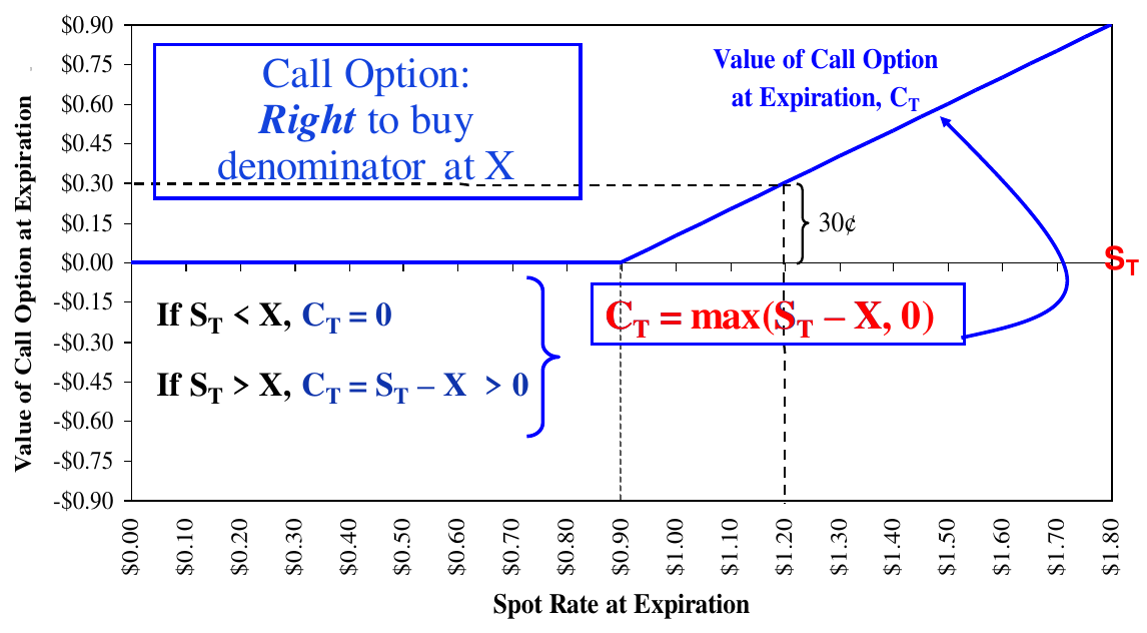

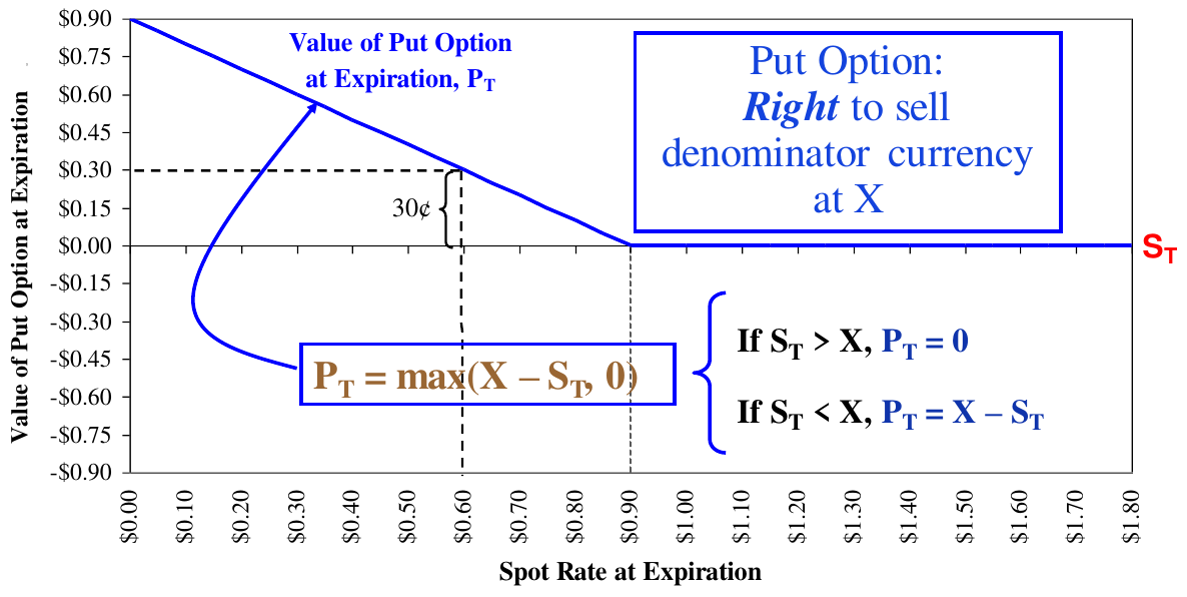

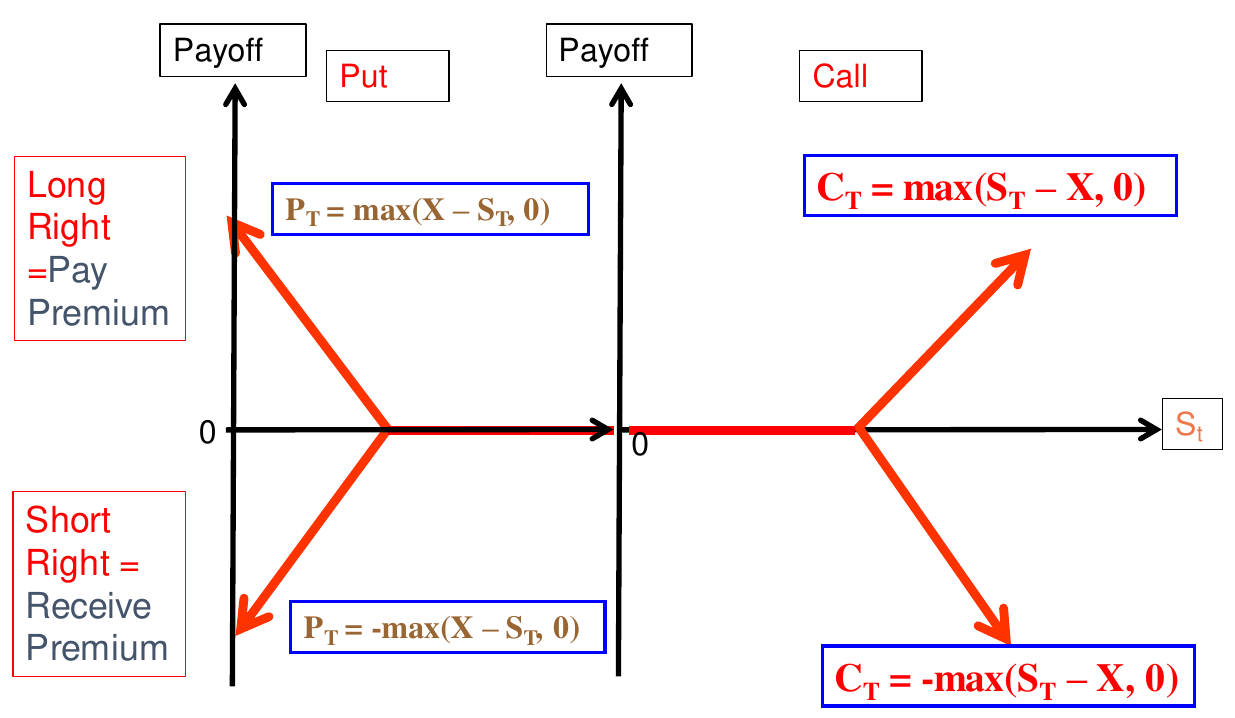

Foreign Currency Options (Call / Put)

Options give the option holder the right, but not the obligation to buy or sell the a specified amount of the underlying asset (currency) at a pre-determined price (exercise or strike price)

Types of Options

- Call: gives the holder the right to buy denominator currency

- Put: gives the holder the right to sell denominator currency

- American option: exercise the option at any time

- European option: exercise only on the expiration date, not before

exercise / strike price (X): the exchange rate at which foreign currency can be purchased (call) or sold (put)

Payoff of Call Option at Expiration (US$/CHF)

Payoff of Put Option at Expiration (US$/CHF)

Long Call CHF = Long Put USD

Long Put CHF = Long Call USD

Intrinsic and Time Value

| Call | Put | |

|---|---|---|

| Intrinsic value | max( - X, 0) | max(X – , 0) |

| in the money | – X > 0 | X – > 0 |

| at the money | – X = 0 | X – = 0 |

| out of the money | – X < 0 | X – < 0 |

| Time Value | C – Int. value | P – Int. value |

C = Call premium; P = Put premium

Factors that Affect Options Prices

- current exchange rate (S): as S↑, Call price↑ and Put price↓

- strike price (X): as X↑, Call price↓ and Put price↑

- time to expiration (T): as T↑, the value↑

- volatility of the exchange rate (σ): the higher the σ of the exchange rate, the greater the value

- domestic interest rate (): as ↑, Call price↑ and Put price↓

- foreign interest rate (): as ↑, Call price↓ and Put price↑

Summary

Put Call Parity:

Swaps

Swap: a contractual agreement to exchange periodic cash flows between two parties

Single currency interest rate swap: One counterparty exchanges the interest payments of a floating-rate debt obligation for the fixed-rate interest payments of the other counterparty. Both debt obligations are denominated in the same currency

Cross-currency interest rate swap: One counterparty exchanges the debt service obligations of a bond denominated in one currency for the debt service obligations of the other counterparty denominated in another currency

TODO

L6 - Transaction and Translation Exposures

Transaction exposure

Transaction exposure - measures gains or losses that arise from the settlement of existing financial obligations (e.g., account receivables, account payables) whose terms are stated in a foreign currency.

Example: firm that has signed a contract to ship goods overseas at a fixed foreign currency price

- €1,800,000, payment to be made in 60 days

- S0 = $0.9000/€

- If the euro weakens to $0.8500/€, then firm will receive $1,530,000 (€1.8mil * $0.85/€)

- If the euro strengthens to $0.9600/€, then firm will receive $1,728,000 (€1.8mil * $0.96/€)

- exposure is the chance of either a loss or a gain

Inflows of FC

- Accounts receivable denominated in a foreign currency (FC)

- Long-term sales contracts denominated in a FC

- Deposits, bonds, or notes denominated in a FC

- Forward purchase of a FC

Outflows of FC

- Accounts payable denominated in a FC

- Long-term purchase con-tracts denominated in a FC

- Loans, bonds, or notes due denominated in a FC

- Forward sales of a FC

Net Exposure by currency and date = Total Inflows – Total Outflows

Value at Risk (VaR)

VaR – To estimate the potential maximum loss (over a certain period) on the value of positions that are exposed to exchange rate movements

Example: A firm has €10m position (receivable). The current spot rate is $1.20/ €. Normal distribution with μ = 0 and σ = 6% per month. What is its VaR?

- x = μ – 1.65 * σ (the 5% tail probability of adverse move starts at 1.65 standard deviation below the mean)

- x = 0 – 1.65 * 0.06 = - 0.099

- VaR = -0.099 * $12m = –$1,188,000

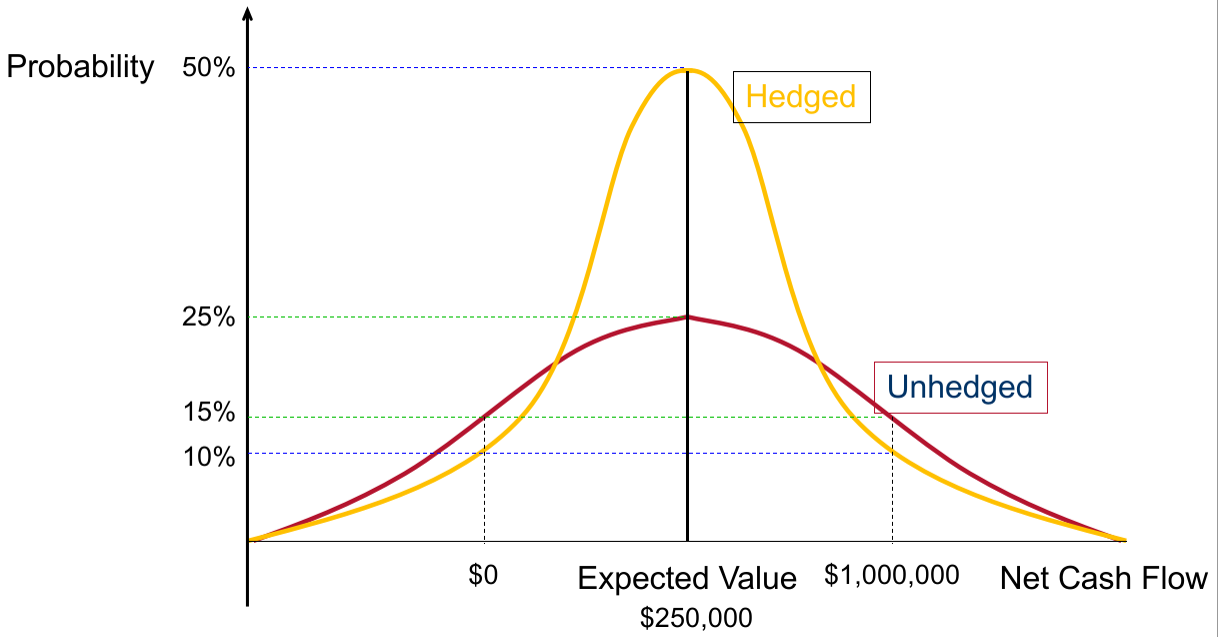

Hedge Strategy

Hedging protects from loss, but also eliminates any gain

Hedging reduces expected tax if taxes are convex rather than linear functions of income

Suppose that income:

- ≤ $10m, tax rate = 20%

-

$10m, tax rate = 40%

Income:

- Good State (50%) = $15m

- Bad State (50%) = $5m

Don’t Hedge, E(Tax) = 0.5 * [($10m * 20%) + ($5m * 40%)] + 0.5 * ($5m * 20%) = $2.5m

Hedge, E(Tax) = 1.0 * $10m * 20% = $2m

Transaction exposure can be managed by

- Contractual Hedges: Forward, Options, and Money Markets

- Operating and Financial Hedges: Risk-Sharing Agreements, Leads and Lags in Payment Terms, Swaps and Other Strategies

Hedging of Receivables

- Sell futures or forward

- Buy Put Option

- Money market hedge

- borrow foreign currency to be received

- convert to domestic currency

- invest for future use (domestic currency)

- Note: Fear of FC depreciating in value

Hedging of Payables

- Buy futures or forward

- Buy Call Option

- Money market hedge

- borrow domestic currency

- convert to foreign currency

- invest for future use (foreign currency)

- Note: Fear of FC appreciating in value

Alternate Hedging Strategies

- Risk Shifting

- Leading and lagging

- leading (accelerate timing of depreciating currency receivables)

- lagging (delay timing of appreciating currency receivables)

- Currency Risk Sharing

- Cross-hedging

- Currency diversification

Note: Options are more flexible hedging devices than forwards and futures in the sense that the forward contract must be exercised

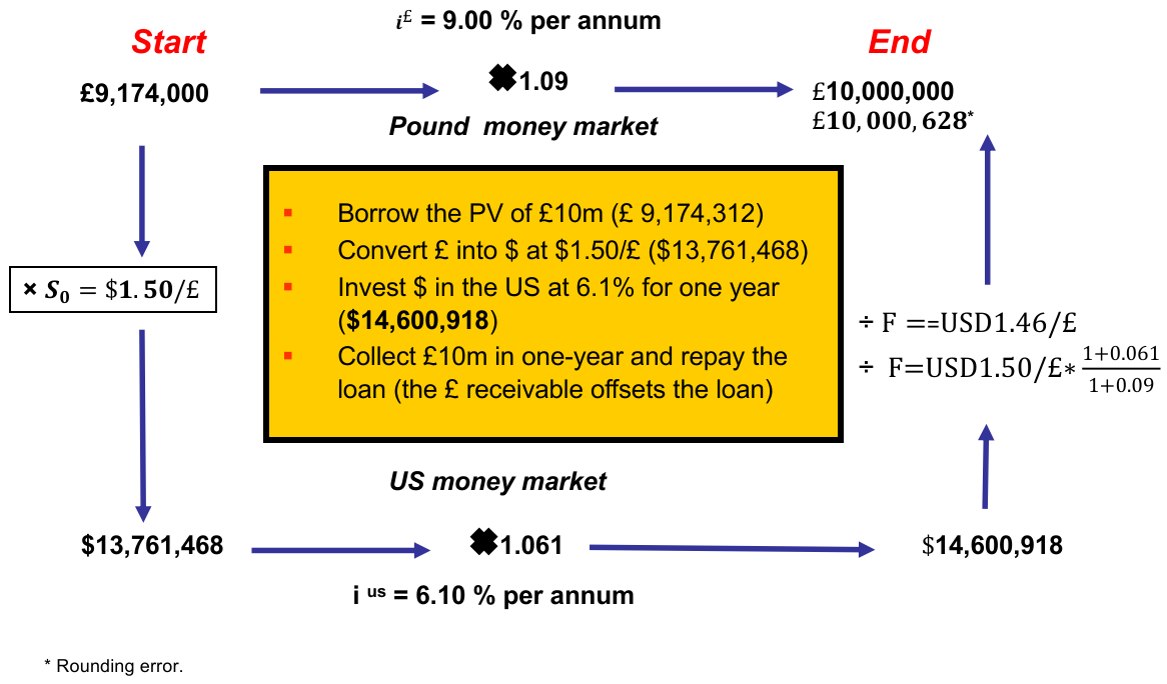

Hedge Example

Assume Boeing is expected to receive 10m GBP (£) in one years time

Available Information:

- one-year forward rate: US$1.46/£

- spot rate: US$1.50/£

- put option on pounds with strike of US$1.46 has a premium of US$0.02

- interest rates:

- US: 6.10% per annum

- UK: 9.00% per annum

IRP:

F = (USD1.50/£) * (1+0.061)/(1+0.09) = USD1.46/£

Forward Hedge

Forward Hedge - By selling GBP forward, Boeing locks in the US$ receivable at $14.6m (£10m * $1.46/£)

Gain/Loss from forward hedging: (F – ST) * FC hedged

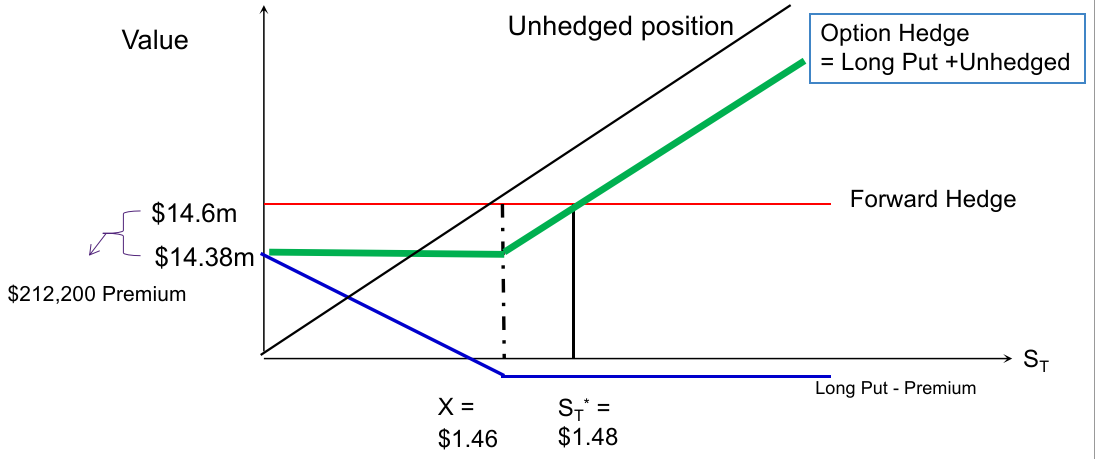

Options Hedge

Options Hedge: Long Put - Has the right to sell £ @ $1.46/GBP

- will receive $14.6m if exercised

Note: A premium of $200,000 (£10m * $0.02) was paid up-front

- We need to take into account time-value of money.

- The upfront cost is actually $212,200 ($200,000 * 1.061) in one years time.

Money Market Hedge

Money Market Hedge - Borrow (or lend) in the foreign currency to hedge its foreign currency receivables (payables)

- match FC assets & liabilities in the same currency

Boeing's Money Market Hedge

- Borrow the PV of £10m at 9% (£ 9,174,312)

- Convert £ into $ at $1.50/£ ($13,761,468)

- Invest $ in the US at 6.1% for one year ($14,600,918)

- Collect £10m in one-year and repay the loan (the £ receivable offsets the loan)

Translation (Accounting) Exposure

For Multinational corporations, financial statements need to be converted into the home currency when consolidated

Accounting Rules for Translation

- Current/Non-current Method

- Monetary/Non-monetary method

- Temporal method

- Assets & liabilities: Translated at the historical exchange rate if they are recorded at historical cost

- Revenue & expense items: Translated at the historical exchange rate or at the average rate if there are multiple transactions of a similar nature

- Current rate method

- Assets & liabilities: Translated at the current exchange rate

- Revenue & expense items: Translated at their historical rates (or at an average rate if there are multiple transactions)

Translation rates:

- Current (exchange) rate

- Historical (exchange) rate

- Average (exchange) rate

The most common way to hedge is a balance sheet hedge in which the company has equal amounts of assets and liabilities in each currency that offset each other and leave the company without any translation exposure.

L7 - Economic Exposure

Economic / Operating Exposure

Economic / Operating Exposure – the impact of currency fluctuations on a firm’s future cash flows

- the extent of sensitivity of the Market Value of a firm (or a portfolio of securities) to exchange rate movements

Cash flows () can be disentangled into its various constituents that can be denominated in several currencies.

This exposure can be denoted as:

where

It measures the marginal impact on firm value by a change in the ($A/FC) exchange rate.

The Source of Economic Exposure

Economic exposure arises when the value of the firm is affected by changes in the Real exchange rate.

Exchange rates affect the value of the firm through their impact on

- Revenues

- Costs and

- Competitive position

Note: if a change in the exchange rate merely reflects differential rates of inflation between countries, then relative prices would not change and the value of the firm would be unaffected

Cash flows can be further decomposed into:

- Sales/Revenues = Price * Quantity

- Costs = Fixed + Variable * Number of goods produced

Conduits for Economic Exposure

Perfectly Elastic Demand: Demand elastic. To maintain market share, absorb all cost increases (no pass-through). Profit margins fall.

Perfectly Inelastic Demand: Demand inelastic, pass-through all cost increases, maintain/improve margins.

Elastic Demand: Demand elastic, absorb some of cost increase, lose both market share and profit margins.

Impact of Exposure can be DIRECT or INDIRECT

- For example, AUD 1/£, HC=AUD; FC=£

| HC strengthens | HC weakens | |

|---|---|---|

| e.g., AUD 0.8/£ | e.g., AUD 1.3/£ | |

| Direct Exposure | ||

| Sales abroad (e.g., sell @ £10) | Unfavourable | Favourable |

| Source abroad(e.g., cost @ £1) | Favourable | Unfavourable |

| Profits abroad | Unfavourable | Favourable |

| Indirect Exposure | ||

| Supplier sources abroad | Favourable | Unfavourable |

| Competitor sources abroad | Unfavourable | Favourable |

Estimating Economic Exposure

Audits / Scenario Analysis: Qualitative examination of the separate elements of a firm’s operating cash flow and anticipating its sensitivity to real exchange rate changes.

Statistical Approach: Regress changes in firm value on changes in exchange rates to obtain a quantitative assessment of sensitivity.

- Presumption is that changes in the value of a firms public securities measures the effect of exchange rate changes. (measure of aggregate exposure)

Managing Economic Exposure

Use of Marketing Strategies

- Market Selection

- Pricing Strategy/Product strategy

- Promotional Strategy

Use of Production Management

- Input mix

- Plant Location & Shifting production among plants

- Raising Productivity (i.e. lowering costs)

Natural Hedges

- Toyota has insulated itself to some extent against dollar fluctuations

- It builds 60% of the cars sold in North America

- Michelin, the world’s largest tire maker, has 40% of its annual sales in North America.

- Most of the imported raw materials used by Michelin are also priced in dollars

- BMW has created natural hedges by producing cars in America and Britain

- It opened a factory in S. Carolina in 1994 and produced 160,000 vehicles there in 2003.

Transactional Hedges

- Unlike BMW, Porsche makes most of its cars in Germany, so its costs are mostly in euros

- Yet a large chunk of revenues come from sales of sports cars in America

- Unlike BMW, Porsche has no natural hedge

- Thus, Porsche uses financial hedging

- Porsche says they are “100% hedged” against the dollar through 2007

(Lack of) Transactional Hedges

- Volkswagen attributed most of its 1.2 Billion euro losses in 2003 to currency swings it had not hedged against

- This had a ‘real effect’ as it announced plans to cut 5000 jobs.

- It has since ‘stepped up its hedging’ to 70% of its exposure. (NY Times Jan. 17, 2004 & Mar. 9, 2004)

L8 - International Diversification

Diversification

- Potential for higher expected returns

- Potential for lower portfolio risk

The Algebra of Portfolio

Assumptions

- Nominal returns are normally distributed

- Investors want more return and less risk as denominated in their home currency

wi = proportion of wealth devoted to asset i such that Si wi = 1

Expected return on a portfolio:

Portfolio Variance: where

Portfolio Variance (2 assets):

The N-asset Case and risk of an equally weighted portfolio:

| American | 14.30% | 16.40% |

| British | 17.60% | 29.90% |

| Japanese | 17.70% | 35.70% |

| A | B | J | |

|---|---|---|---|

| A | 1 | 0.557 | 0.325 |

| B | 0.557 | 1 | 0.317 |

| J | 0.325 | 0.317 | 1 |

Example: Equal weights of A and J

- = (1/2)(0.143) + (1/2)(0.177) = 16%

- = (1/2)2(0.164)^2 + (1/2)(0.357)^2 + 2(1/2)(1/2)(0.325)(0.164)(0.357) = 0.0481

- = (0.0481)^(1/2) = 21.9%

Key Results of Portfolio Theory

- Reduced risk depends on correlation of assets in portfolio

- As the number of assets increases, portfolio variance becomes:

- more dependent on the covariances (or correlations)

- less dependent on variances

Internationalising a Domestic Portfolio (A multiple-asset case)

TODO Charts

Return on International Investments

The realized dollar return for an Australian resident (HC:AUD) investing in a foreign market (FC:Yen) is given by:

- : local currency return in the market (Japan)

- : change in the exchange rate between the local currency (AUD) and the foreign currency (Yen)

Total Return

An illustration with Japanese stock

- US investor takes $1,000,000 on 1/1/2002 and invests in stock traded on the Tokyo Stock Exchange (TSE)

- On 1/1/2002, the spot exchange rate was ¥130/$

- = ¥130m

- The investor purchases 6,500 shares valued at ¥20,000 for a total investment of ¥130m (6500shares @ ¥20k)

- At the end of the year, the investor sells the shares at a price of ¥25,000 per share yielding ¥162.5m (6500shares @ ¥25k)

- On 1/1/2003, the spot exchange rate was ¥125/$

- ¥162.5m / ¥125/$ = $1.3mil

- The investor receives a 30% return on investment

- Returns in USD = ($1.3m - $1m) / $1m = 30%

Or use the formula:

- = (¥25,000 / ¥20,000) - 1 = 0.25$

- = (1/¥125) / (1/¥130) - 1 = 0.04

- = (1 + 0.25)(1 + 0.04) - 1 = 0.30

International Diversification

Domestic International Mutual Funds

- Savings on transaction and information costs

- Circumvention of legal and institutional barriers to direct portfolio investments abroad

- Professional management and record keeping

Country Funds

- invests exclusively in the stocks of a single county

- Speculate in a single foreign market with minimum cost

- Construct their own personal international portfolios

- Diversify into emerging markets that might be inaccessible to individual investors

Diversification Multinational Corporation (MNC)

- Multinational firms with operations across countries (Coca-Cola, GMs)

- Cash flows are influenced by country factors and local economies

American Depository Receipts (ADRs)

- Foreign stocks often trade on US exchanges as ADRs

- It is a receipt that represents the number of foreign shares that are deposited at a U.S. bank

- The bank serves as a transfer agent for the ADRs

Exchange Traded Funds (ETFs): investment companies registered with the SEC, with assets consisting of baskets of securities included in an index fund

- Designed to track an index

- One share in an ETF provides an investor diversification to all the constituents of the relevant index, and its price and yield track the indices performance

- An open end fund that trades like a stock

- Low cost, convenient way for investors to hold diversified investments in several different countries

BRICs: “mutual fund” that invests in Brazil, Russia, India and China

Sharp ratio & Diversification: Some Results

TODO

Home Bias Puzzle

Home bias: portfolio investments are concentrated in domestic equities

TODO Chart